Q1 '24 Digest

How's it going?

Here's a sneak peek at our new logo, masterfully designed by the incomparable Kneil Melicano (check out more of his work here). He’s busy crafting our upcoming website, set to launch soon! We’re very excited.

Reports Performance

Mood: 😃

Valero

Our thesis for investing in Valero rested on three key principles:

It’s an exceptional company with high returns on capital, a long-term investment outlook, and a commitment to rewarding shareholders.

It’s an inflation hedge from the demand side, through its exposure to rising consumer activity.

It is protected from geopolitical instability, given that most of its assets are in the U.S.

Back in January, we wrote:

“By thinking about [Valero] as a defensive play against either supply-side shocks or a prolonged inflationary period fueled by a robust consumer, we align our strategy more closely with specific risk management objectives, rather than getting lost in the broader and highly speculative task of attempting to accurately nail down market-wide trends.”

So far, all three points have unfolded broadly as expected, and the stock initially gained > 40% before falling back to end up +22%.

For the quarter, Valero reported strong results despite extensive maintenance across its refining system. Its sustainable aviation fuel (SAF) project in Port Arthur is ahead of schedule and now expected to be operational by the fourth quarter of 2024. This project positions the company as a leading SAF manufacturer globally.

Refining margins were supported by tight product balances, influenced by seasonally heavy maintenance across the industry and geopolitical events. Ukrainian drones have been targeting Russian refineries with a good deal of success, even when such facilities are located hundreds of miles within Russian borders.

Valero expects margins to continue being supported by low product inventories and strong demand. According to COO Gary Simmons:

“This year was the year where you had kind of a peak in terms of new capacity additions. And then from this point forward, you get to where global petroleum demand outpaces new refinery capacity additions significantly, and we see several years of tightness.”

Vinci

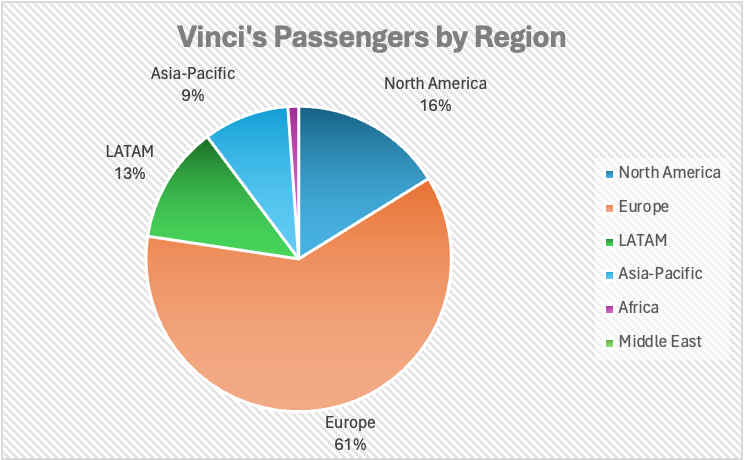

The day after we published our report, Vinci announced it was acquiring a 50% stake in Edinburgh airport, the sixth busiest in the UK, serving 14 mn passengers in 2023. Half of 14 mn amounts to about 3% of total airport traffic managed by Vinci.

Excluding the Edinburgh acquisition, which has yet to close, we calculated Vinci’s airport traffic by region:

Then, using ACI’s global traffic data, we calculated Vinci’s share of overall global traffic to get a sense of market share. At 2.6%, Vinci has a lot of room to grow over the next decade in airports concessions.

Overall, consolidated revenue in Q1 grew by 4.8% y/y (4.2% organically), with a rise in order intake and a record-high order book, ensuring good visibility and operational selectivity for future projects. Assuming Vinci's internal metrics are robust and reliable, this should be a tailwind for margins.

For comparison, nominal GDP in the Eurozone for Q1 was 2.9% (real GDP of 0.3% + CPI of 2.6%).

Concessions: Revenue up 6.6% y/y, with Autoroutes facing disruptions from farmer protests in January, but ultimately minimal traffic decline, while Airports saw a robust increase in passengers due to new routes and sustained demand.

Energies and Cobra IS: Both reported strong revenue growth (5% and 7.5% y/y respectively) and record order books, highlighting strength in international markets and renewable energy projects.

Construction: Moderate revenue growth (3.9% y/y) with a strong order book, driven by high activity in France and stable operations abroad.

2024 Guidance:

Growth Expectations: Vinci anticipates revenue growth across most business lines, with particular strength expected from Cobra IS and continued recovery in airport passenger numbers.

Operational Margins: Expected to maintain or improve, despite potential negative impacts from new taxes.

We are very satisfied with these results and have continued to increase our position in Vinci. We see a solid long-term outlook for the company, as well as medium-term favorable factors, including:

- An increase in GDP and easier financial conditions within the Eurozone.

- Exposure to key infrastructure, especially in building and maintaining power grids, renewables, and data centers.

Hershey

This quarter, the main story surrounding Hershey and other confectioners has been the meteoric rise in cocoa prices, which have since moderated slightly. We view any pullback in Hershey stock (to below $180) as a buying opportunity, considering that the high cost of cocoa, which is dollar-denominated, will impact buyers outside the U.S. significantly more than it will Hershey. Going forward, reduced demand in emerging markets could further realign cocoa prices closer to normal levels.

Here’s CEO Michele Buck on the topic:

“We have robust processes in place to ensure continuity of supply and good visibility into our costs. We are well covered for 2024 and do not expect recent volatility to affect our financial outlook for the year.”

For Q1, Hershey reported net sales growth of 8.9% y/y—though out of this amount, 7% was attributed to additional inventory that was strategically built up in anticipation of switching over to a new ERP system. Underlying business growth was 1.9% y/y, which is in-line with full-year expectations.

In the North American confectionary segment, without inventory accumulation, sales growth was 1.4%—of which +6% was from price realization and -4.5% from volume. So it seems price increases have significantly affected demand.

Gross margin was a healthy 44.9%.

The content provided by Quits & Starts, including all materials on this website, in the newsletter, and in any other communication from its author, is strictly for informational and educational purposes. It is not intended to be, and should not be interpreted as, investment, legal, or any other type of advice. Readers are encouraged to conduct their own research and due diligence. It's important to remember that investment decisions should be tailored to an individual's specific financial situation, goals, and risk tolerance.