Greggs Plc

Britain's Best Food-to-Go on Sale

Investing can sometimes feel like tracking prey through dense jungle—following patiently at a distance, waiting for the right moment to emerge from the bush and pounce.

We’ve been tracking Greggs (LSE:$GRG1) for some months now. It appears to be one of those rare, prized elks: a great franchise at a reasonable price. Yet, lately, its stock price has been stumbling and limping along for reasons that seem disconnected from fundamentals.

Greggs is a leading UK food-on-the-go retailer with a vertically integrated supply chain and a growing nationwide footprint. It operates ~2,500 shops, including franchised locations (which now account for 20% of the overall “estate”).

Greggs serves affordable bakery products such as sausage rolls, pastries, sandwiches, salads, and beverages, appealing broadly across demographic segments due to convenience, brand recognition, and above all, value.

The fact that the company owns its production bakeries and distribution centers allows it to deliver consistent quality and to control costs more efficiently than peers who have to rely on external suppliers. With its emphasis on everyday low pricing, Greggs has established itself as a value leader—a strategy that proved especially effective during the recent cost-of-living crisis. This positioning may once again prove advantageous should the UK slide decisively into recession (which for now does appear to be the direction the country is headed in).

Greggs is led by CEO Roisin Currie (since 2022) and CFO Richard Hutton, who oversee a clear growth strategy centered on expanding the number of UK stores beyond 3,000 by 2026. The recent surge in Capex includes buildout of new production and distribution capacity to handle this future store growth.

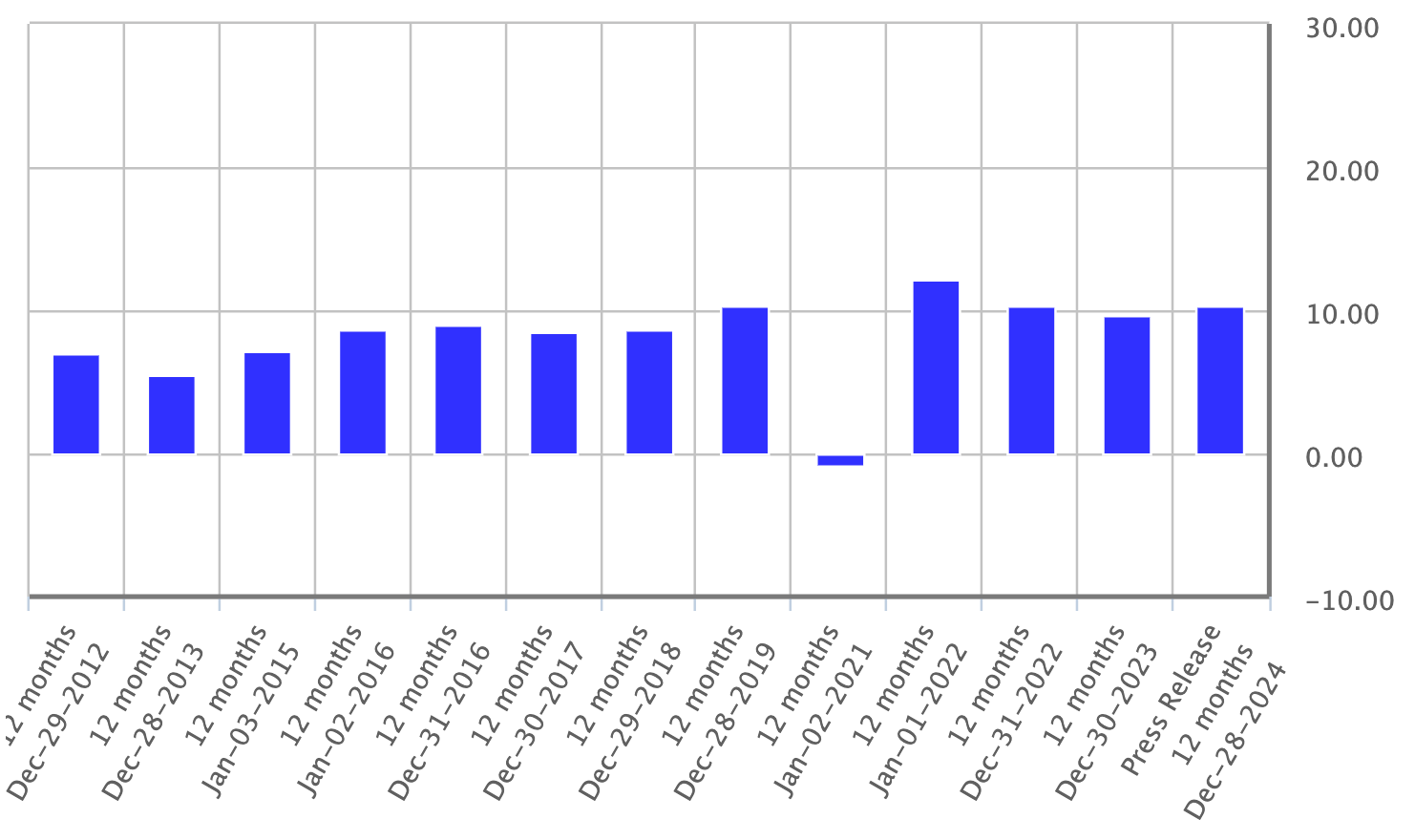

So far, management’s strategy has been working. Since 2016, revenue has grown at a CAGR of 11%, making Greggs now one of the largest foodservice chains in the country by outlet count. For context:

The company’s format spans high streets, travel hubs, petrol forecourts, retail parks, and even drive-thrus and supermarkets, following a strategy of being accessible in both traditional and non-traditional locations.

This kind of reach has turned Greggs into the UK’s leading breakfast destination, now capturing 19.6% of all food‑to‑go breakfast visits and unseating McDonald’s from the top spot (keeping in mind that Greggs has many more locations than McDonald’s). It also ranks among the country’s largest coffee sellers—recently cited as #3 by volume, ahead of Starbucks.

Scale, however, brings the eventual risk of UK market saturation. We don’t think Greggs is there yet, especially with management pushing new growth levers by keeping shops open for evening meals and scaling up digital and delivery channels—and early results suggest these initiatives are working.

There’s also another possible tailwind for profit margins and ROA: Because franchise units account for roughly 1/5 of Greggs’ current estate but around 1/3 of all new openings, the store mix is shifting toward a capital‑light model. Franchise partners fund the build-out, pay staff and rent, while Greggs books high‑margin wholesale sales and royalty income with minimal operating expenses.

While international expansion could be a future avenue for growth (providing a huge runway if they ever crack a model for Europe or elsewhere; yet prove costly if it misfires), there’s no indication it’s anywhere on the roadmap, so the growth story for now is firmly UK-centric.

In terms of valuation, the company is trading at a 13x Fwd P/E multiple, 0.8x P/Sales, and 3x P/Book. Like-for-like sales growth has cooled sharply, which may explain part of the discount, but we see it as a reversion to a more normal rate—not a sign of serious underlying weakness in the business.

For the next 5 years, we estimate a sustainable revenue growth rate of 7-8%, which includes 2% from same-store sales growth (driven by price realization, expansion into evening hours, and delivery), 1% same-store growth from franchises2, and 5% from new stores3.

A Buffett-style back-of-the-envelope “DCF” gives us a 55% upside from here.

At this valuation, Greggs’ long‑run cash‑flow outlook looks very compelling on a risk‑adjusted basis. While we’re still evaluating our options to reduce FX exposure with futures (we’ll write another post on that soon), we’ll be initiating a 5% portfolio position tomorrow.

All materials produced by Reveles Research, LLC—whether posted on this site or distributed elsewhere—are supplied solely for information and education. Nothing herein constitutes, or should be construed as, investment, legal, or any other professional advice. You should carry out your own analysis and due diligence before acting. Every investment decision ought to reflect your unique financial circumstances, objectives, and tolerance for risk.

For investors, the London-listed stock ($GRG) generally offers better liquidity and trading conditions. Platforms providing access to international markets, such as Interactive Brokers, facilitate this. The ADR ($GGGSY), by contrast, tends to have lower liquidity and wider spreads.

Management reported FY24 like‑for‑like sales of 7.4% in franchised outlets (a data point they hadn’t revealed before). With franchises making up roughly 20% of the estate, that translates to about a 1.5% lift to total LFL growth. For prudence, we round that down to 1% in our model.

If we assume that Greggs will get to ~3,000 stores in 3 years (as per management’s guidance), that’s a 20% growth over that period which translates into 6% growth pa. If we assume they get there in 5 years, instead of 3, then that’s 4% growth pa. A midpoint of 5% seems like a reasonable assumption.