LKQ Corp

Dependable biz, 8x P/FCFE, potential sale upside

Here’s a good business with solid fundamentals going for cheap.

LKQ is a distributor of car repair parts. These parts are sourced and sold wholesale, usually to repair shops and dealerships through its distribution centers. Unlike its peers, Autozone and O’Reilly, LKQ does not operate its own retail store network.

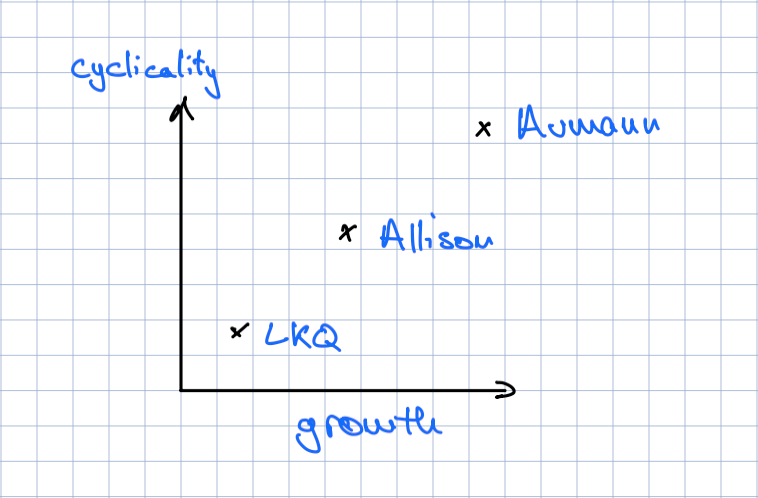

In broad terms, LKQ operates in the vehicle aftermarket industry. We’ve invested in and written about a few different auto-adjacent companies. Interestingly, each occupies a distinct position in the industry’s value chain:

Aumann sells equipment to automakers that are building EV production lines. The long-term demand case is strong: if the industry is moving toward EVs, automakers will need to invest in the machinery required to produce them. But that demand is tied to capital spending plans which makes the business inherently very cyclical.

Allison Transmission sits closer to current production. It sells transmissions to truck manufacturers, so demand is driven more by present truck sales than by automakers’ investment plans. That makes the business less speculative and less cyclical than Aumann’s, but the growth outlook is also more moderate. Traditional transmissions might be valuable today, especially in commercial vehicles, but they are not the future.

LKQ sits at the other end of the spectrum. It has low growth prospects but a very large installed base of old vehicles on the road which regularly need maintenance and repair. This is an unsexy but dependable industry.

We see value in all three companies (at the prices we bought them) for different reasons. LKQ is currently trading at an 8x price-to-free-cash-flow multiple. It has consistently paid out a good dividend and bought back stock. The yield on those combined is currently > 6%.

But what does LKQ do? Basically it buys or salvages spare parts (oil, filters, windshield wipers, brakes, paint and body materials, remanufactured engines, etc) and sells them on through its distribution network. It has large operations in the US, Canada, and Europe.

LKQ deals mainly in what are called “alternative parts” which consist of non-OEM parts (knock-offs, essentially) along with genuine parts recovered from salvaged vehicles. This is interesting to us because it means LKQ is serving older, cheaper cars—a segment that’s more insulated from EV adoption.

In this sense, LKQ is not primarily exposed to frontier auto technology. Rather, it is exposed to the installed base: the enormous population of vehicles already on the road, many of which will continue to need repair long after new-car sales have shifted to EVs.

It is still unclear what effect EVs will actually have on LKQ’s business. The obvious negative is that they do not have traditional engines, transmissions, or many of the related mechanical parts that are valuable categories for the company today.

Management, being management, gives the transition a positive spin and calls it a tailwind. According to their reasoning, EVs are more electronically complex and their batteries are likely to become a valuable component in the salvage stream. If LKQ can safely recycle these new parts, they say, then the company can gain from higher-value categories. We remain skeptical.

But, again, LKQ’s business draws from the quantity of vehicles on the road, not new-vehicle sales. EVs can grow rapidly as a share of new sales and still take many years to become a meaningful share of repairable vehicles.

The fact that organic growth has been weak recently has added to the negative sentiment. In the immediate post-Covid period, LKQ’s organic sales growth was unusually strong, averaging roughly 6% per year from 2021 to 2023. Since then, however, it turned negative, running at about -2% per year.

In the North America segment, the reasons for this are twofold. The first involves insurance premiums, which sky-rocketed after Covid. When premiums rise, drivers reduce coverage and often can’t afford to make repairs out of their own pocket. This reduces the demand for parts.

The second reason involves used car values. After an accident, there are two options: either repair the damage or send the totaled car to the junkyard. On average, the higher the value of the car, the more likely it is to be repaired. From 2022-24 values plummeted by about 25%.

In Europe the situation is different. Volume pressure there seems to be coming from aggressive discounting. Management has acknowledged that some pressure was self-inflicted through introductory private-label pricing, while saying most of the weakness was market-related.

Nonetheless, we believe all these problems are temporary and will soon stabilize. Growth in North America was just about flat in Q1 2026.

Overall, LKQ’s business is relatively easy to understand. It is not a high-growth business, but it is a necessary one, and that gives it a degree of dependability that is attractive to us.

There is also a potential catalyst. Earlier this year, the board announced it was reviewing strategic alternatives, including a possible sale of parts or of the whole company. Given where the stock has traded, any concrete evidence of a credible buyer could drive meaningful upside for shareholders.

In terms of valuation, the company is trading at a 12% FCF yield. Free cash flow is the appropriate measure of earnings power because it doesn’t include a large amortization of intangibles charge (customer/supplier relationships) which is a vestige from past acquisitions and not an ongoing expense.

We have taken a full position at a price below $26.

All materials produced by Reveles Research, LLC—whether posted on this site or distributed elsewhere—are supplied solely for information and education. Nothing herein constitutes, or should be construed as, investment, legal, or other professional advice. You should carry out your own analysis and due diligence before acting. Every investment decision ought to reflect your unique financial circumstances, objectives, and tolerance for risk.