Why Greggs Reminds Me of Zara

And Why That Makes Me Bullish

This is a second article in a series on $GRG. For the first, click here.

This weekend, on the plane back from seeing Buffett retire from running Berkshire, I was listening to a podcast about Inditex, the parent of Zara, which told the story of how the company became the leader in fast fashion by building a business model that turns speed into a structural advantage.

Zara famously relies on tight vertical integration, controlling design, manufacturing, and logistics—meaning new clothing designs can move from idea to store shelves in a matter of days. This structural advantage limits inventory risk, reduces markdowns, and improves working capital.

It reminded me of something I’d read recently, and the thought sent me off looking for the passage: Earnings call. FY 2019. Greggs. The outgoing CEO had articulated a similar principle:

“The fact we’ve invested to centralize production means we can… move more quickly to reformulate products and achieve both new products and sustainability objectives.”

In the same exchange he highlighted that the business is “vertically integrated unlike many others,” a point repeated at the October 2021 Analyst Day when management noted that supply-chain capacity must grow “because we’re vertically integrated— not many people are.”

And that’s when I realized Greggs is trying to be the Zara of food.

Greggs owns nearly every major step between sourcing of raw ingredients and sale of finished products in stores. Unlike most other quick-service food chains1, it operates its own production facilities, logistics hubs, and distribution fleet. Vertical integration on this scale enables Greggs to respond to shifting consumer tastes by introducing new menu items, faster. It also reduces reliance on third-party suppliers, improving cost efficiency and inventory management2.

The market tends to view Greggs primarily as a mature bakery chain, but we wonder if this perspective might not be underestimating how adaptable the company’s integrated structure really is. A higher menu refresh rate may keep customers continuously coming in, and leave competitors behind.

Here’s a recent timeline of Greggs’ menu innovation (2019-2025).

January 2019 – Nationwide launch of the vegan sausage roll following earlier success with a vegan Mexican bean wrap, signalling the start of Greggs’ plant-based programme.

January 2020 – Roll-out of the vegan steak bake and the first vegan doughnut; vegan hot-cross buns added in March.

August 2021 (H1 2021 call) – New vegan Ham & Cheeze Baguette, a vegan breakfast sausage and the Vegan Sausage, Bean & Cheeze Melt.

March 2023 (FY 2022 results) – Evening-focused six-slice pizza box goes nationwide; “Hot Yum Yums” with dipping sauces debut; two rice-salad meal boxes introduced, including the vegan Sweet Potato Bhaji option.

August 2023 (H1 2023 call) – Launch of a healthy flatbread range, vegan Mexican chicken-free bake, hot wraps and the first trials of over-ice drinks; management notes “customers are loving them.”

July 2024 (H1 2024 call) – Over-ice drinks available in 500 shops (target 700 by year-end); introduction of a smaller four-slice pizza box, expansion of salads and flatbreads, and pilots of fish-finger wraps and sandwiches alongside made-to-order hot chicken wraps (>200 shops).

March 2025 (FY 2024 pre-recorded call) – Over-ice drinks range now in 1,175 shops with more flavors planned; ready-to-drink canned lattes launched; made-to-order chicken and fish-finger wraps rolled out to >200 shops; evening menu broadened with a BBQ Chicken & Bacon pizza, four-slice pizza box, and the first hot Mac-and-Cheese meal solution.

This sequence shows the steady cadence (and breadth of offerings) supported by Greggs’ in-house manufacturing and daily frozen distribution. Recognizing such a structural advantage increases our confidence in the company’s long-term growth prospects (putting international expansion perhaps a little less out of reach).

The comparison to Zara is, of course, not a perfect one—customer tastes in fashion are decidedly more fickle than in food. But there are certainly similarities that we are starting to appreciate.

Below we take a closer look at some basic metrics for Zara ($ITX), Greggs ($GRG), and Domino’s UK ($DOM).

Gross Margins

Greggs’ margin is highest because cheap ingredients, daily sell-through and full ownership of production leave little cost inside “cost of sales.” Inditex earns a still-healthy but lower margin because fabrics, sewing labour and fashion markdowns are inherently costlier. Domino’s sits lowest because, on the group P&L, it functions as an ingredient supplier whose revenues embed far less mark-up over raw commodity costs.

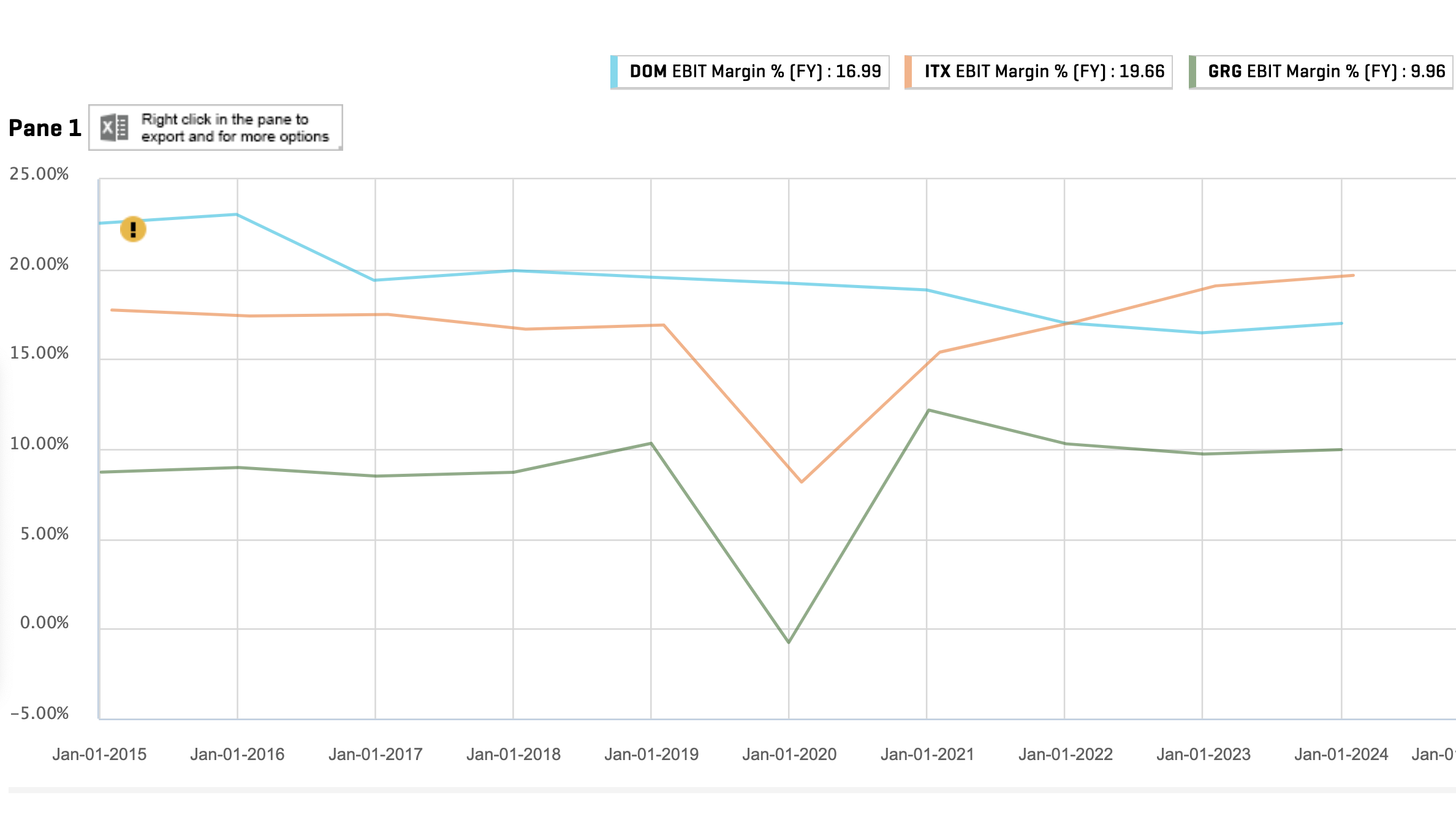

EBIT Margins

Domino’s posts the highest EBIT margin because it has outsourced the expensive parts of retailing to franchisees while keeping the royalty and logistics mark-up on its own books. Inditex earns a solid mid-teens-to-20 % margin thanks to fast-fashion pricing power, but full store ownership means a heavier SG&A load than Domino’s. Greggs converts the richest gross margin of the trio into the lowest EBIT margin because its value positioning relies on high in-house labour, distribution and depreciation, all of which sit below the gross-profit line and weigh on operating profit.

Fixed Asset Turnover

Domino’s converts the most revenue per pound of fixed assets because franchisees, not the group, own the expensive retail equipment. Inditex sits in the middle: big sales, but it carries billions of store leases on its own balance sheet after IFRS 16. Greggs turns assets the slowest because its model deliberately holds factories, lorries and leases to keep unit costs low—capital intensity is the flip side of that vertical-integration advantage.

As these charts illustrate, Greggs’ business model appears to have more in common with Inditex than with Domino’s.

We’ll be writing more about Greggs soon… 5/5/25

All materials produced by Reveles Research, LLC—whether posted on this site or distributed elsewhere—are supplied solely for information and education. Nothing herein constitutes, or should be construed as, investment, legal, or other professional advice. You should carry out your own analysis and due diligence before acting. Every investment decision ought to reflect your unique financial circumstances, objectives, and tolerance for risk.

Domino’s Pizza operates its own dough production facilities and controls key aspects of distribution logistics, though not as extensively as Greggs. Chipotle centrally prepares much of its food and maintains relationships with farms and suppliers. In-N-Out Burger in the U.S. manages its own meat processing plants, bakeries, and distribution centers. Pret A Manger in the UK operates central kitchens for daily food prep. However, Greggs’ level of end-to-end ownership remains unusual, giving it uniquely high flexibility when compared to most competitors.

From 2024 Annual Report: “A key part of this is the evolution of our supply chain operating model. In 2016, we began to move away from a traditional regional bakery model – where every site made every product – towards a consolidated, centralised approach. Today, our nine production facilities are manufacturing centres of excellence, specialising in specific products and producing them at scale. Our plans for further growth will require additional capacity in our supply chain over the coming years. During 2024, we introduced a fourth savoury line at our Balliol Park site in Newcastle upon Tyne, increasing production capacity for savoury rolls and bakes by circa 35%, and completed work on expanding our Radial Distribution Centres in Amesbury and Birmingham providing 300 additional shops of logistics capacity. We also set in motion two major new development projects: a new frozen manufacturing and logistics facility in Derby (due to open in 2026) and a new National Distribution Centre in Kettering (due to open in the first half of 2027). Both sites are designed to support our Radial Distribution Centres and will significantly increase our logistics capacity; when both are operational we will be able to service an additional 700 shops through the automated upstream picking of frozen, chilled and ambient goods, taking our total logistics capacity to 3,500 shops.”